Your Sales Figures In Danger Of Matching Zoom Share Price Performance?

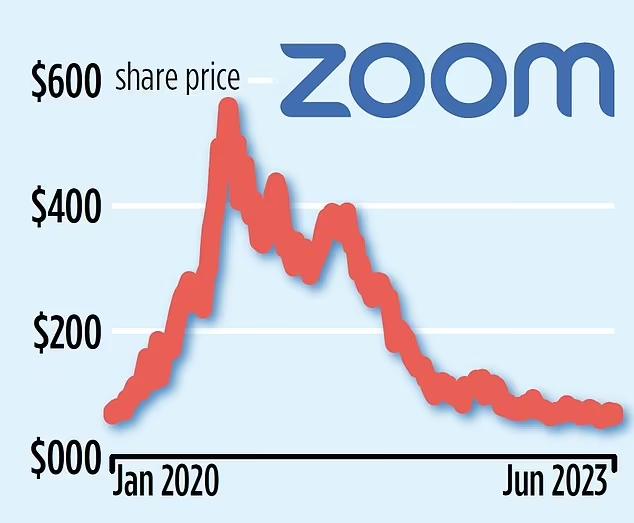

Above is the online dailymail graphics team linegraph of Zoom's share price over the past 42 months.

It accompanies current revenue stall at around $4½bn and profit growth deceleration down to maybe ~3pc.

I think I can just about make out a trader tell of the 'head and shoulders'. A pattern apparently suggesting that upon seeing three sets of peaks and troughs, with a larger peak in the middle, a stock's price will likely begin falling. Although in Zoom's case, the left shoulder seems higher than the head, but still.

We all know why the soaring rise. But then why the drop off, plummeting all the way back down to where they were?

And before you say it, 'coronavirus' is not an answer.

No.

Let's make the assumption that back in early-20, Zoom were the First Mover. Eventhough they were not the world's first videolinkers. Yet they were (pace Skype/WebEx/NetMeeting) the first to be readily serviceable from 'home'. And Boom.

It took a couple of years. Coincidentally arriving as lockdowns ceased. But avaricious competitors spying the end of the economist rainbow of super-normal profits eventually got their acts together.

Chief among them, Microsoft. From which Teams is an unmitigated calamity for live video working, and selling in particular. It being so inappropriate for the task, it's scary that so many honest sellers are forced by their IT colleagues to be handicapped by mandating such ill-suited tool. Imagine if we made them use only a Nokia 3310 for work...

Beyond the Big Bill wonky world of Windoze, other big players stirred. It also took a while, but Google's combinations and reworks for their subsequent Meets mops up plenty of video hours.

A raft of niche players also sprouted. Mini apps for specific use cases. And then there's the growing native rush. Programs already in the workflow space (and beyond) slotting in seamless video capability.

All contributing to the decline of Zoom. Relative, mind you. As at 31 December 2019, they reported active daily user numbers of around 10 million people. By 2023, that was now stated as 300 million. A figure strangely appearing the same as that touted mid-20.

My point to consider; is this flatline because Zoom failed to adapt?

And if so, then how much is your selling struck by a similar oversight?

How have you progressed your video selling since those, if not sepia-tinged the perhaps pixelated, days of 2020?

If you've made no conscious effort to work on how selling is different over video than by phone, in-person or prose, then there I suggest is a significant contributory reason why your sales graph may unwelcomely echo Zoom stock.

Time to move your line upwards?