Adapting to Endure

Here's one semi-randomly selected chirp. Chin-stroking upon a major Venture Capitalist musing of our time. Namely Sequoia Capital's recent what you might label 'SOSA', or State of the Startup Address. Which takes the form of a slidedeck with accompanying 52-page speaker notes pdf. The below is from a Danish 'cellular automoton' posting inside Y-combinator, no less;

These slides feel surprisingly like a twitter-style blog sequence. . .

Somehow, I feel like I’m being served ads.

By a [VC].

Walk away.

Then there's the bank tech pros [long read]. Who feel this 'crucible moment', though 'not a time to panic' (rather 'pause and reassess', really), treatise is really all about finance pressures they themselves will face from twin pincers of rising costs of capital and valuation compression.

Thirdly, consider this pair of summary paragraphs from the weekly Telegraph business column of Andrew Orlowski;

"One of the oldest VC firms in Silicon Valley, Sequoia Capital, has now issued a gloomy 52-page prospectus for its startups with a name reminiscent of those nuclear fallout advice pamphlets from the cold war, like Protect and Survive. In Adapting to Endure, the firm warns:

“We do not believe that this is going to be another steep correction followed by an equally swift V-shaped recovery like we saw at the outset of the pandemic”.

That may seem a bit rich from the firm that once backed Google’s creepy spywear, Glass, and which recently auctioned off an NFT. But we are all better off when the silly money stops flowing, and to be honest, better off without the fools who shower cash at fools, like Sequoia."

One tweeter even suggested this deck was simply a rehash of their pre-GFC one, which earned them praise back in 2008.

As you can likely judge from these, sympathetic critiques for said presentation feel thin on the ground.

For our Solution Sell slant, I'll draw tips first from structure.

Consider their flow;

If you buy into the septet sectional slicing, then 4/7ths is devoted to the Before. The remaining 3/7ths, the After.

That's roughly a 57-43 split.

Do the maths, and find that in format alone, they focus for a third longer on how we got here, over where we want to go.

In terms of slides, discarding placeholders and title slides, then each 'half' I'd say feature 19 slides each. The After including 3 illustrating an AirBnB case study. Yet given the volume of notes, the Before looks like it would be the lengthier of the stanza pair to fit the aforementioned proportion.

Many an old hand may call this decent wallowing.

Yet this scene-setting is so essential in getting the audience to truly feel you understand their world, that I remain aghast at how seldom it is covered in the kind of weighting we see here.

As for content, in general, I feel there's a few decent pointers in this deck for our use. Here's three.

They cite five 'famous' sayings in among the messaging. Four of which stem from dead people. Too many for us. Sales pitches should really only have quotes from those involved, very much alive and present.

I'd also highlight the ability to coin, get adopted and so own, the 'pitch' through your own unique contribution to the bid syntax.

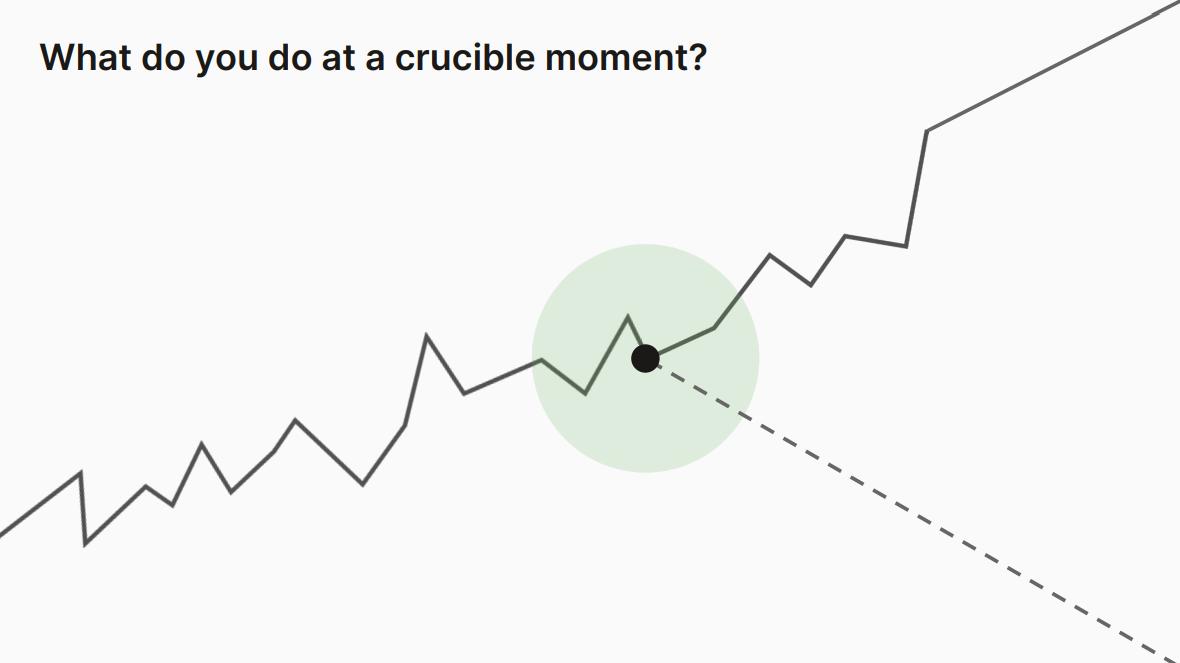

Sequoia's here being the p28 labelling of a "crucible moment";

The graphic and construct both hit.

Lastly, this concluding slide is worthy of asterisk.

Strategies for Uncertain Times

○ Simplicity scales, complexity doesn’t

○ Speed - one of the greatest business strategy

○ Double down on your top talent

○ Seek alignment, not agreement

○ Tighten up value proposition/solve real problems

■ Three reasons why people buy regardless of market conditions (enterprise POV):

● Drive growth ● Save money (real, hard ROI) ● Reduce risk ● Everything else is fluffy

Mark closely that last line.

At the Enterprise level, which of that trio do your prospects want/need your help with? Drive growth, save real money, or reduce risk?